UBI

Arguments for a Universal Basic Income

Contents

- Introduction

- The Accountant: Simple Tax Code

- The Realist: Demonstration of Viability for the UK

- The Conservative: Less Bureaucracy, More Responsibility

- The Libertarian: Freedom from Gouging

- The Liberal: Less Vilification of the Poor

- The Socialist: A Robust Safety Net

- The Capitalist: Removal of Market Distortion

- The Entrepreneur: More Stability

- The Economist: Effective Stimulus

- The Philosopher: The Land Dividend

- Conclusion: Implementation Possibilities

- (Appendix I: The United States)

- (Appendix II: Comments & Clarifications)

Introduction

The concept of a Universal Basic Income is one that goes beyond the more general idea of “Benefits” or “Welfare”. Payments from the government to the poorest in society have long been the norm in developed economies; indeed, whilst it was a novel concept when Sir Thomas More published his “Utopia” in 1516, the following half millennium has seen his arguments become quite mainstream. He writes:

“Petty larceny isn’t bad enough to deserve the death penalty. And no penalty on earth will stop people from stealing, if it’s their only way of getting food.”

However, most of these payment systems come with some sort of limitation, usually quite reasonable sounding: they may be means tested, so that the less poor you are, the less you get; they may be dependent on how much you have paid into them previously, more like a savings plan or employment insurance; they may not pay anyone that has a job, as these people need it less; or they may require you to spend all of your savings before you receive any payments, as if you have savings, you do not need assistance.

As the name suggests, Universal Basic Income is a payment system that is based around universality – the same payment is to be made to everyone in the country, rich or poor. Whether someone has a job or not, has paid into a scheme or not, has savings or not, the government pays them the same amount. This is aimed at replacing most “Welfare” payments, which would no longer be needed if the Universal Basic Income were enough for everyone to survive on. It is not designed to replace any government payments that deal with disabilities or healthcare, only those related to survival such as housing benefit, state pensions, unemployment benefit and so on.

The first person to articulate the concept of what we now refer to as a Universal Basic Income was Thomas Paine in 1796. Since then however, it has been supported by a surprisingly wide range of figures, including the philosophers John Stuart Mill and Bertrand Russell, progressive economist Henry George and conservative economist Milton Friedman. That it has received support from so many people with such diverse political viewpoints suggests that there may be many different perspectives from which it may be argued as a beneficial policy. Despite this, it has not yet been implemented on a country-wide scale anywhere in the world.

Over the next few sections, I hope to address any controversies and lay out several arguments that advocate for a Universal Basic Income from a variety of different viewpoints, to demonstrate that it is indeed an idea of merit regardless of which political opinions you may hold.

The Accountant: Simple Tax Code

In countries that try to have a progressive tax system, income taxes can be exceedingly complicated. The tendency is to try not to tax people very much when they are earning less than a certain amount, then to increase the percentage that their income is taxed at, as that income increases. This is seen as preferable to taxing everyone at the same rate, as although 20% of a £10,000 income is much less than 20% of a £100,000 income, that £2,000 is essential for the first person to be able to eat, whereas the person earning £100,000 could spare a lot more than £20,000 before even noticing the difference.

To take the UK as an example, in the 2018-19 tax year, the first £11,850 of your annual income is not taxed, then anything received above that is taxed at 20%. Anything above £46,350 had an additional 20% tax applied (called the 40% or higher rate band), and anything above £150,000 had a further 5% applied (called the 45% or additional rate band). This is further complicated by the fact that for every £2 of income over £100,000 that you earned, you lose £1 of the tax free £11,850, which is then taxed at 40%, resulting effectively in any income between £100,000 and £123,700 being taxed at an additional 20% (a notional 60% band).

Finally, to make matters even more confusing, there is Employee’s National Insurance – an income tax in all but name, which is an additional 12% on any income between £8,400 and £46,350, and an additional 2% on anything above that. Expressed in a table, this looks as follows:

| Lower Income Threshold | Upper Income Threshold | Income Tax Rate | NI Rate | Combined Tax Rate Applied Within Band |

|---|---|---|---|---|

| £0 | £8,400 | 0% | 0% | 0% |

| £8,400 | £11,850 | 0% | 12% | 12% |

| £11,850 | £46,350 | 20% | 12% | 32% |

| £46,350 | £100,000 | 40% | 2% | 42% |

| £100,000 | £123,700 | 60% | 2% | 62% |

| £123,700 | £150,000 | 40% | 2% | 42% |

| £150,000 | + | 45% | 2% | 47% |

There are a great many resources such as online tax calculators that help to make sense of all of this, but what I am interested in here is the “effective tax rate”, that is, if you were to apply the same rate to all of your income to come up with your tax bill, what would that rate be.

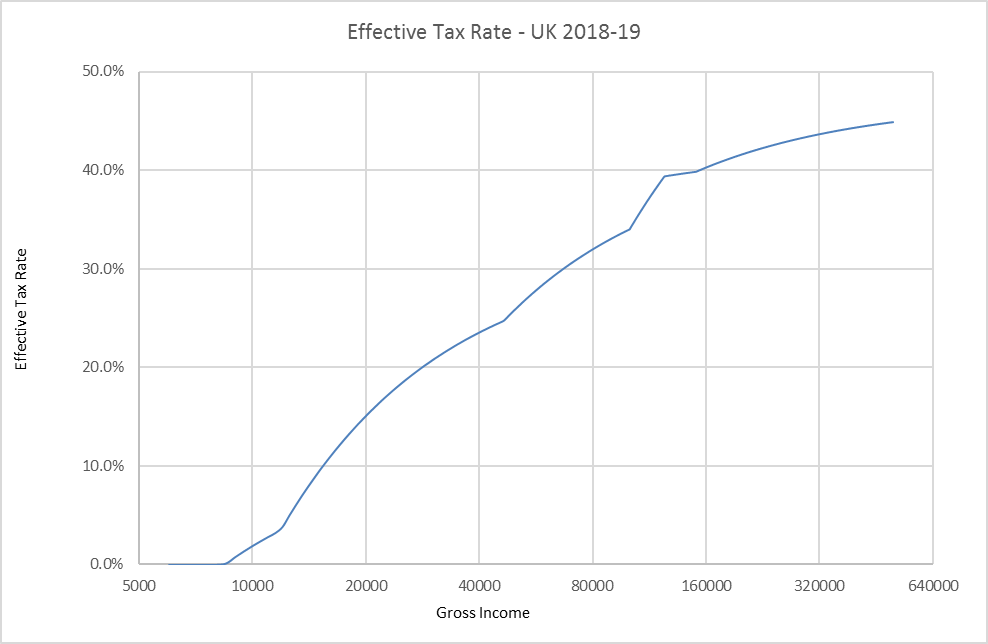

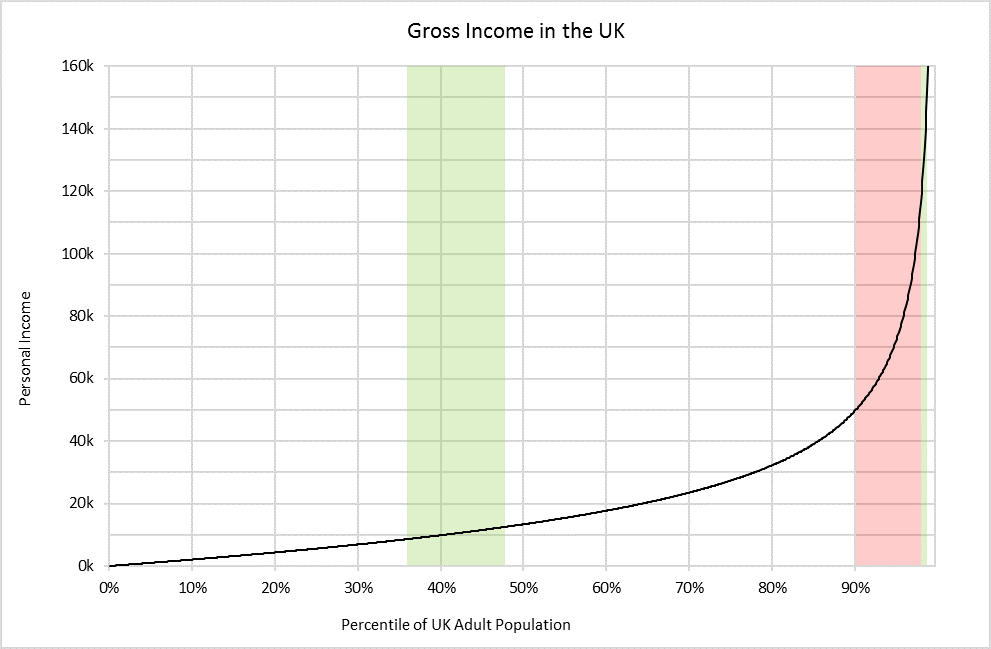

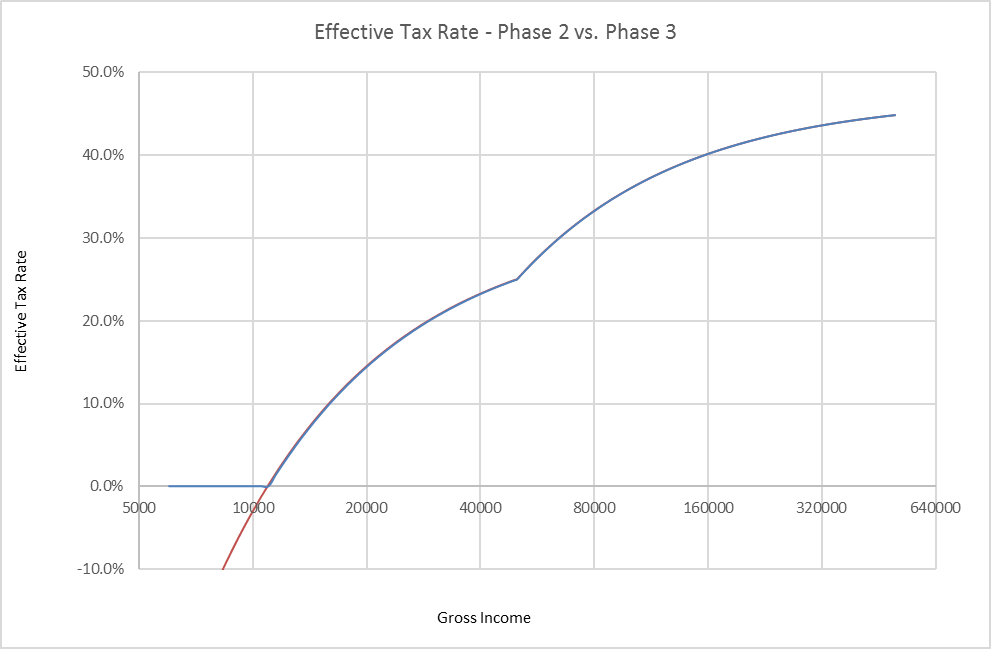

The results of the UK income tax code are shown as a blue line on the graph below (plotted on a logarithmic x-axis – doubling with each successive gridline rather than increasing a fixed amount, so that it is easier to see the detail):

The gross income is the amount paid before tax, and the impact of the thresholds mentioned above, mean that someone earning £20,000 per year will pay £3,022 in tax, for an effective tax rate of 15.1%, while someone earning £80,000 will pay £25,587 in tax, for an effective tax rate of 32.0%. The strange kinks in the line are a direct result of the discontinuities in the tax bands, but the intention is clear – to tax higher earners at a higher rate than lower earners, this being the definition of a progressive tax.

Whilst much simpler, clearly taxing everyone at the top rate of 47% (45% plus 2% National Insurance) on all their income is not ideal, as this would be an enormous financial burden on people with lower incomes, and would be a huge tax increase for everyone except people earning well into the seven figures. What happens when we combine it with a Universal Basic Income however?

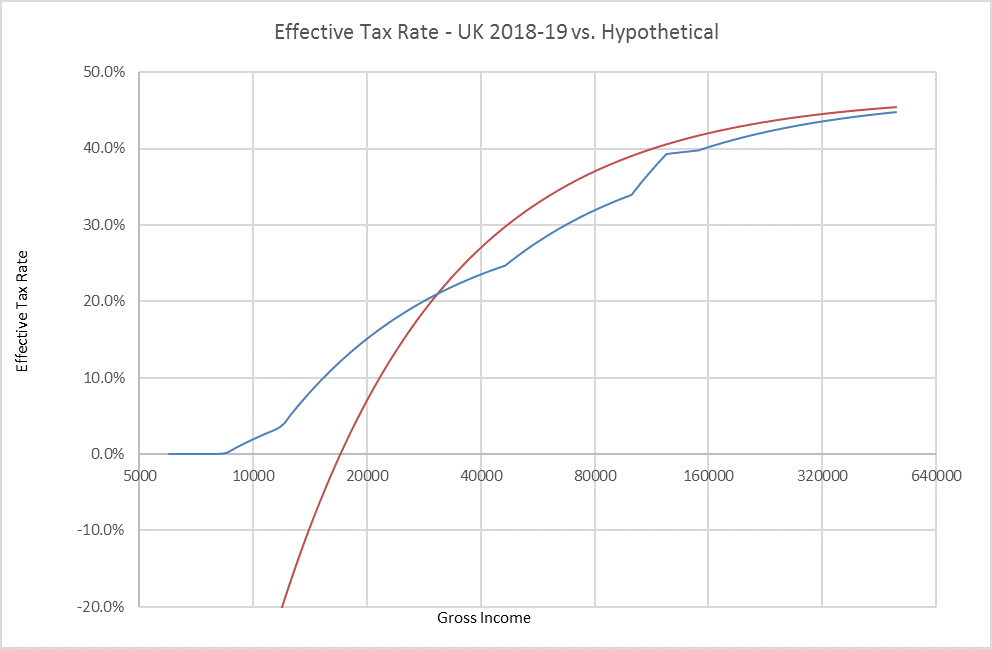

The red line on the graph below shows the effective tax rates under a hypothetical tax code which taxes all earned income at 47%, but also pays a Universal Basic Income of £8,000 per annum. As you can see, rather than a flat line across the top at 47%, which would be the result without a Universal Basic Income, the combined effect of a flat tax rate and a Universal Basic Income gives rise to a similar shaped curve to the one produced by the exceedingly complicated UK tax code:

There are a few key things to note here:

- The effective tax rate for someone earning £17,000 per annum is 0% – they are paying tax at 47%, which is £7,990, but they are receiving a Universal Basic Income of £8,000, so the net effect is that they pay no tax.

- Anyone earning less than this has a negative effective income tax rate – someone earning £10,000 per annum will be paying £4,700 in tax, but receiving £8,000 in Universal Basic Income, for a net income of £13,300, or a tax rate of -33%.

- At about £31,000 per annum the two tax codes result in about the same amount of tax. Under the UK system, you get the first £8,400 untaxed, between £8,400 and £11,850 is taxed at 12% for £414, between £11,850 and £31,000 is taxed at 32% (20% plus 12%) for £6,128, giving a total of £6,542 or an effective tax rate of 21.1%. Under the hypothetical system, all £30,000 is taxed at 47%, for £14,570, and then Universal Basic Income of £8,000 is received, giving a net tax bill of £6,570, or 21.2%.

- Above this point, the hypothetical tax code does result in a higher tax rate. Someone earning £40,000 per annum would see their effective tax rate increase from 23.6% to 27.0% – an increase in tax of £1,378, or £115 per month, while someone earning £80,000 per annum would see an increase from 32.0% to 37.0% – an increase in tax of £4,013, or £334 per month.

- The lines are both approaching 47% as incomes increase. Neither line will ever reach exactly 47%, but the impact of the lower tax brackets or the Universal Basic Income become less and less significant as the gross income increases.

With just two numbers, 47% and £8,000, it was possible to define a tax code that is progressive, understandable and fairly similar to the existing UK code. Furthermore, it is difficult to argue that this code is unfair, as it is not punitively targeting high earners with very high tax rates – both numbers apply to everyone, at every income level.

This rather neatly demonstrates the counterargument to the oft raised objection that “Only people who need it should get state assistance”, and “paying money to the rich is a waste”. When viewed together with the tax code, it becomes clear that a Universal Basic Income is effectively a reduction in tax for anyone with a positive effective tax rate. If it is deemed that the rich are not paying enough tax after factoring in the Universal Basic Income, then the tax rate can be increased, but in this scenario, anyone earning over £31,000 has already seen a net tax increase, so these people are definitively not “being paid extra money”. The impact of a Universal Basic Income on anyone with a positive effective tax rate (here, people earning over £17,000) is simply to change their effective tax rate. Certainly, they will be receiving payments from the government, but they will also be paying taxes, so it will be the change in the total amount of money they take home at the end of every month that they care about.

The benefit for the government in operating this way is simplicity – by paying everyone in the country, and taxing everyone in the country, there is no need for entire government departments devoted to means testing, nor is there a need to perform a calculation any more complicated than multiplying two numbers together, to work out how much tax to charge. It might seem inefficient for the government to be paying someone money only to recoup it back as tax, but transferring money is an incredibly simple and quick thing to do. Checking that a calculation is correct, and verifying that exactly the right amount has been received or paid is the thing that takes time and effort, which makes it a good idea to reduce the amount of complexity in the calculations as much as possible, even if it does mean doubling the number of transactions.

The Realist: Demonstration of Viability for the UK

It is a complaint often made about a Universal Basic Income, that it would be impossible to finance. Using the UK as an example, I will demonstrate that this is not the case, by estimating the likely actual cost of such a programme, showing that it is in fact no more unrealistic than the system of state benefits in place now. I have used the UK government’s statistics for the financial demographics of the UK.

The key figures forecast for the 2018-19 financial year are set out in the table below:

| Range of total income (lower limit) | All taxpayers | Total income of taxpayers | Tax liability |

|---|---|---|---|

| £ | Number | £million | £million |

| 11,850 | 4,090,000 | 54,800 | 1,130 |

| 15,000 | 6,170,000 | 107,000 | 6,130 |

| 20,000 | 8,520,000 | 209,000 | 20,000 |

| 30,000 | 8,010,000 | 305,000 | 37,800 |

| 50,000 | 3,220,000 | 214,000 | 42,800 |

| 100,000 | 558,000 | 66,800 | 19,600 |

| 150,000 | 181,000 | 31,000 | 10,400 |

| 200,000 | 191,000 | 55,200 | 20,500 |

| 500,000 | 37,000 | 24,900 | 9,860 |

| 1,000,000 | 13,000 | 16,900 | 6,740 |

| 2,000,000+ | 6,000 | 26,200 | 10,400 |

| Total | 30,996,000 | 1,110,800 | 185,360 |

This shows that there were 30,996,000 tax payers in the UK in 2018, who in total contributed £185 billion of income tax. This table does not include Employee’s National Insurance, which makes a significant contribution to the government’s tax revenues, but this can be calculated using the thresholds mentioned in the previous section.

The following table does this, however these calculations are only an estimate, as they ignore the fact that some of these people’s income may be from pensions, on which no National Insurance is paid, they ignore people earning between £8,400 and £11,850 that pay National Insurance but no Income tax, and they ignore the slightly different National Insurance payments made by the self-employed, but none of these should cause the numbers to be out by enough to make a meaningful difference.

| Range of total income (lower limit) | All taxpayers | Average Income | Estimated Average NI Payable | Total National Insurance |

|---|---|---|---|---|

| £ | Number | £ | £ | £million |

| 11,850 | 4,090,000 | 13,399 | 600 | 2,453 |

| 15,000 | 6,170,000 | 17,342 | 1,073 | 6,621 |

| 20,000 | 8,520,000 | 24,531 | 1,936 | 16,492 |

| 30,000 | 8,010,000 | 38,077 | 3,561 | 28,526 |

| 50,000 | 3,220,000 | 66,460 | 4,956 | 15,959 |

| 100,000 | 558,000 | 119,713 | 6,021 | 3,360 |

| 150,000 | 181,000 | 171,271 | 7,052 | 1,276 |

| 200,000 | 191,000 | 289,005 | 9,407 | 1,797 |

| 500,000 | 37,000 | 672,973 | 17,086 | 632 |

| 1,000,000 | 13,000 | 1,300,000 | 29,627 | 385 |

| 2,000,000+ | 6,000 | 4,366,667 | 90,960 | 546 |

| Total | 30,996,000 | 78,047 |

When added to the first table’s £185 billion, this gives us a total government revenue of £263 billion across Income Tax and Employee’s National Insurance, which is summarised below:

| Range of total income (lower limit) | All taxpayers | Total income of taxpayers | Tax liability | Total National Insurance | Net Tax Contribution |

| £ | Number | £million | £million | £million | £million |

| 11,850 | 4,090,000 | 54,800 | 1,130 | 2,453 | 3,583 |

| 15,000 | 6,170,000 | 107,000 | 6,130 | 6,621 | 12,751 |

| 20,000 | 8,520,000 | 209,000 | 20,000 | 16,492 | 36,492 |

| 30,000 | 8,010,000 | 305,000 | 37,800 | 28,526 | 66,326 |

| 50,000 | 3,220,000 | 214,000 | 42,800 | 15,959 | 58,759 |

| 100,000 | 558,000 | 66,800 | 19,600 | 3,360 | 22,960 |

| 150,000 | 181,000 | 31,000 | 10,400 | 1,276 | 11,676 |

| 200,000 | 191,000 | 55,200 | 20,500 | 1,797 | 22,297 |

| 500,000 | 37,000 | 24,900 | 9,860 | 632 | 10,492 |

| 1,000,000 | 13,000 | 16,900 | 6,740 | 385 | 7,125 |

| 2,000,000+ | 6,000 | 26,200 | 10,400 | 546 | 10,946 |

| Total | 30,996,000 | 1,110,800 | 185,360 | 78,047 | 263,407 |

From this we can see that despite earning less than the minimum wage full time, the people in the first row still contribute over £3.5 billion in taxes on their income (£7.83 per hour, 8 hours a day for 240 days per year is £15,034 per annum).

The final piece of information that we need is the cost of the existing state benefits that are provided. This is also published by the UK government.

The forecast figures for the 2018-19 financial year, published in the autumn of 2018, consist of a total of £182 billion administered by the Department for Work and Pensions (DWP), and a further £37 billion that is administered elsewhere.

As will be mentioned in the next section, “The Conservative” – any benefits for disabilities or health purposes should be administered by relevant healthcare professionals, which would mean that in the UK’s case, they would be transferred to the National Health Service. These disability-related benefits are the following:

| Personal Independence Payment |

| Disability Living Allowance |

| Attendance Allowance |

| Industrial injuries benefits |

| Severe Disablement Allowance |

| Mesothelioma |

| Pneumoconiosis 1979 |

| Armed Forces Independence Payment |

| Specialised Vehicles Fund |

After removing these from our review, we are left with a list of the state benefits that a Universal Basic Income would be aimed at replacing. Some of these are rather small, so have been combined together into “Other Benefits” in the list below, however the largest of these (coming in at around 50% of the total) is the State Pension. Importantly, this does not include pension schemes payable to government employees, as these do not fall into the category of welfare – these are effectively private pensions, where the pension fund happens to be run by the government.

| State Benefit | £million |

|---|---|

| State Pension | 96,620 |

| Child Tax Credit and Working Tax Credit (non-DWP) | 25,073 |

| Housing Benefit | 23,955 |

| Employment and Support Allowance | 15,881 |

| Child Benefit & One Parent Benefit and Guardian’s Allowance (non-DWP) | 11,161 |

| Pension Credit | 5,042 |

| Carer’s Allowance | 3,228 |

| Jobseeker’s Allowance | 2,526 |

| Statutory Maternity Pay | 2,520 |

| Income Support | 2,184 |

| Winter Fuel Payments | 1,979 |

| Bereavement related benefits | 496 |

| Over 75 TV Licences | 468 |

| Maternity Allowance | 448 |

| Tax Free Childcare (non-DWP) | 239 |

| Financial Assistance Scheme | 229 |

| Other Benefits | 644 |

| Total | 192,693 |

This tells us that the system that we are trying to replace generates £263 billion in tax revenues, and spends £193 billion of this on state benefits, giving a net contribution to the government’s revenues of £70 billion. As a side note, this £193 billion figure does not include the costs of administering these benefits, which could result in additional cost savings.

With this information, we can now calculate the equivalent figures under a system with a Universal Basic Income. I shall base this on the same system outlined in the last section – “The Accountant” – a flat tax of 47% on all earned income, and a Universal Basic Income of £8,000 to every adult in the country. It is worth noting at this point that £8,000 per annum is very similar to the UK state pension it is looking to replace, of £164.35 per week (2018 figure, coming to £8,546.20 for the year), meaning that people shouldn’t lose out too much under this change of approach.

Per UN estimates, the UK population was approximately 66,700,000 in 2018, and 18.8% were under-16. The adult population was therefore approximately 54,200,000. This can be incorporated into the taxpayer figures used above, to calculate how many adults paid no tax. The results of these calculations are in the table below – the tax liability column is the total income multiplied by 47%, while the Universal Basic Income column is the number of taxpayers multiplied by £8,000:

| Range of total income (lower limit) | All taxpayers | Total income of taxpayers | Tax liability | Universal Basic Income | Net Tax Contribution |

|---|---|---|---|---|---|

| £ | Number | £million | £million | £million | £million |

| 0 | 23,204,000 | 0 | 0 | 185,632 | -185,632 |

| 11,850 | 4,090,000 | 54,800 | 25,756 | 32,720 | -6,964 |

| 15,000 | 6,170,000 | 107,000 | 50,290 | 49,360 | 930 |

| 20,000 | 8,520,000 | 209,000 | 98,230 | 68,160 | 30,070 |

| 30,000 | 8,010,000 | 305,000 | 143,350 | 64,080 | 79,270 |

| 50,000 | 3,220,000 | 214,000 | 100,580 | 25,760 | 74,820 |

| 100,000 | 558,000 | 66,800 | 31,396 | 4,464 | 26,932 |

| 150,000 | 181,000 | 31,000 | 14,570 | 1,448 | 13,122 |

| 200,000 | 191,000 | 55,200 | 25,944 | 1,528 | 24,416 |

| 500,000 | 37,000 | 24,900 | 11,703 | 296 | 11,407 |

| 1,000,000 | 13,000 | 16,900 | 7,943 | 104 | 7,839 |

| 2,000,000+ | 6,000 | 26,200 | 12,314 | 48 | 12,266 |

| Total | 54,200,000 | 1,110,800 | 522,076 | 433,600 | 88,476 |

Again, this is an estimate, as some of the 23 million people in the zero-income bracket will have part time jobs, meaning that their total income is not zero. It is currently difficult to find out what this income is however, so it is prudent to treat it as zero, to avoid overstating the tax that will be received.

As you can see, the total net tax contribution is £88 billion, after the Universal Basic Income has been subtracted from the government’s tax revenue. This is very similar to, and in fact slightly higher than the £70 billion that we calculated was contributed by the current system of taxes and benefits.

Looked at a different way, summing the positive and the negative figures in the Net Tax Contribution column separately gives us £281 billion in net tax revenue from people that earn over £17,000, and £193 billion in net payments to people earning less than this amount. These figures are readily comparable to the £263 billion in tax revenue and the £193 billion in state benefits that are paid under the current system.

This shows that the “impossible to finance” argument is not accurate – far from needing to “print money” to pay for it, the system of Universal Basic Income demonstrated above is remarkably similar to the existing system in terms of net contribution to the country’s finances, whilst having many other positives, which will be detailed in subsequent sections. With that argument out of the way, the rest should be just tweaking around the edges – from the UK having a population of 54,200,000 over-16s, 12,500,000 under-16s and a combined countrywide gross personal income of £1,110.8 billion, we can calculate that:

| Every £500 of UBI given per person over-16 | will cost £27.1 billion |

| Every £500 of UBI given per person under-16 | will cost £6.3 billion |

| Every 1% of tax applied to personal incomes | will raise £11.1 billion |

Armed with this knowledge, we can go on to investigate alternative policies quickly and easily. Should the Universal Basic Income and tax rate both be higher? £9,000 and 50% would reduce the net contribution to £68 billion. Should children under-16, or families caring for them be eligible for some additional Universal Basic Income? £3,000 per annum for each of the 12,500,000 under-16s in the UK would cost an additional £38 billion. Neither of these render the system fundamentally unaffordable, but more importantly, visualising and discussing these concepts has become far more intuitive, due to the simplicity of the system.

The Conservative: Less Bureaucracy, More Responsibility

In modern times, there seems to be a consensus in economically developed countries, that some form of social safety net is called for. The extent of it may be a matter of significant debate, with conservatives preferring minimal intervention and others desiring more, but it is uncontroversial to say that at some level, one is needed. From the fact that it can take time to find a new job if one finds oneself unemployed, to the fact that industries change, and people need to update their skill-sets to remain employable, there is a well-accepted need to balance “survival of the fittest” with compassion and dignity. The intention of this section is not to convince anyone that some level of state assistance is required, as those believing that this is not the case are likely very few in number; but instead to extol the virtues of a Universal Basic Income from a “small government” conservative perspective, over other more mainstream forms of state assistance programs.

The bureaucracy present in systems of state funded assistance for people with low incomes is renowned. In the UK there are tens of thousands of people employed across the country to ensure that the right people get the right amounts of money from the right places. There are payments for housing assistance, pensions for the elderly, stipends for those out of work, and many other pots of money that are all managed separately, for different purposes. With the notable exception of assistance for the disabled, which is a health-related benefit, dependent on the severity and impact of the disability, and which should arguably be administered by bodies of health professionals (such as the NHS in the UK), all of these benefits could be combined into one Universal Basic Income payment, payable to all. This would reduce the administrative overhead to virtually nothing, because there would be no need to police any arbitrary cut-off points, any phasing in or out of income, or any means testing to ensure that no-one was getting any more than they were entitled to.

This reduction in administration also helps to reduce the size of government, cutting the number of people it employs, and cutting its interference into people’s private lives. One of the limitations of receiving housing benefit in the UK, is that when in a house-sharing scenario, if the person you are sharing a house with has an income, you are only eligible for the benefit if you are not deemed to be in a relationship with them. This limitation might make some sense if the people living together were married, and had therefore agreed in the eyes of the law to be treated as co-dependent, but the limitation is far stricter than that, hinging on whether or not people share a bed. This not only raises issues around people becoming trapped in abusive relationships, but also could be seen as a gross over-reach of the government into the private lives of individuals.

Of course, the Universal Basic Income goes further than removing any strange limitations such as being in a relationship with a cohabitee. Even married couples would be eligible, meaning that a stay-at-home spouse would still be entitled to this income regardless of how much their partner earned. This has the advantage of providing such people with a measure of financial independence, and ensuring that people do not become trapped in a physically or financially abusive relationship. This has the effect of reducing the financial impact of one parent leaving their job to care for children, without needing any special tax breaks aimed at married couples or families.

Another impact of having a Universal Basic Income, with no associated bureaucracy, is that it would allow people to do charitable work or volunteering, without needing to work a second job or have a financial backer (such as a parent or spouse). The issue with current state benefit systems is that the bureaucracy can take a lot of effort to deal with. Meeting the requirements to continue claiming these state benefits can become like a job in its own right, taking up time that could be spent on more productive activities. This would empower those who wanted to contribute to society through volunteer work, as they could be secure in meeting the basics required for survival, whilst also having all of their time to devote to the causes of their choice.

Arguments that “jobs give people meaning in their life” should not be an argument against a Universal Basic Income, as the presence of a Universal Basic Income in no way prevents people from getting jobs. In fact, one of the key principles behind the idea of “small government conservatism” is that people know what is best for themselves, and that the government generally does not know better. This can be borne in mind when considering whether jobs are giving people meaning – if under a system of Universal Basic Income, people take the opportunity to be more discerning about the jobs they want to do, we should trust their judgement. If this does remove some workers from the job market, this will actually make it easier for those people that want to work to find work. This should allow more people to find meaning in their life – people that get meaning from working will find it easier to get employment, and those that find their meaning elsewhere are freer to pursue that instead.

One of the key criticisms of existing state benefit programmes is that they discourage financial responsibility. If someone has saved money for years, then loses their job, it is a common stipulation of state benefits that they may only claim if their savings are below a certain level. This means that they must first use up most of their hard-earned savings, after all, it is argued, why should the government pay them when they can still afford to support themselves? The issue here becomes clear however, when we consider a person who earned the same amount, and spent it all, not saving anything. This person upon losing their job, would become immediately eligible to receive such benefits. The person who was more abstemious and financially responsible is effectively punished in comparison with their contemporary, which effectively discourages fiscal responsibility. Why should someone responsible, that thinks about their future get less than someone irresponsible? The beauty of the Universal Basic Income is that this perverse motivation not to save does not exist. The person that saved money will receive the same government assistance as the person that did not, so although the person that was irresponsible will still be able to get by, the saver will be able to live much more comfortably.

In line with the ideals of both freedom and personal responsibility, the replacement of housing specific benefits makes it no longer a consideration for the government, what housing they should be willing to pay for. Under existing rules, there are criticisms from both directions – some people are forced to move from houses they are comfortable in, because the government deems them too expensive, while other people do not think the government goes far enough, and would prefer that people are moved to less expensive accommodation more proactively. A Universal Basic Income removes the government interference here entirely – if someone would prefer to live with an extra room, and is happy to sacrifice other expenditure for this, they can do so, while equally, if someone is happy to live in smaller accommodation, they may benefit from additional disposable income. People are then free to make decisions based on their own unique circumstances. This applies equally to which town or city they live in – someone determined to live in an expensive part of town is responsible for finding a way to afford this, while someone happy to move to the countryside is likely to find themselves able to live more comfortably. There is no fundamental right never to have to move house, it is a personal decision.

It is often argued that benefit systems contribute to a dependence on the government. The above argument demonstrates how this can be the case, by discouraging prudent behaviour; by requiring too much of someone’s time to navigate, preventing them from exploring more productive avenues; or simply by trapping them in poverty, by reducing benefits too quickly when employment is found, making it uneconomic to work and thus preventing them from improving their lot by moving up the employment ladder. Thankfully the Universal Basic Income does not encourage this kind of dysfunctional behaviour. The only people dependent on the government are those people temporarily in great need, for whom the Universal Basic Income is the only thing stopping them from being out on the street, not “professional” benefit claimants, trying to get the most out of the system, as there is no system to be gamed, and no more money to be claimed.

It can naturally still be argued that there would be some people content to sit at home and subsist on the Universal Basic Income. This would likely be a meagre existence, with very little disposable income once housing, food and heating have been paid for. The vast majority of people strive for more than this, aiming to improve their living situation beyond such ascetic constraints, so the number of people seeing their motivation fall due to a Universal Basic Income should be low.

The Libertarian: Freedom from Gouging

Price gouging is a specific type of market failure that occurs when someone’s life is at stake. As an example, in drought conditions, even though water may quite legitimately be expensive, it is possible for a water seller to make even higher profits than this, due to the desperation of the people in question. If they had the time to shop around, they might be able to buy water at the (albeit expensive, due to the shortage) market rate, but they do not have time – they are dying of thirst, so would give the water seller the deeds to their house if it meant not dying. There is a similar problem with money – ultimately in modern society we need money to survive. It is essential for food, water and shelter, and without it your life is at risk. People in desperate need of money are willing to do all sorts of things that they ordinarily wouldn’t even consider.

There are a great many jobs and activities that are considered by some to be distasteful, dangerous or both, and yet there are still people that do them. The issue is whether they are happy to do the job, simply considering it less distasteful than most, or being more comfortable with the risk than most. The alternative is that they are being coerced into doing it, which would mean that their freedom is being infringed upon. Whilst no individual is threatening them by putting a gun to their head, a person is still being coerced into doing something when the alternative is death, or at the very least, putting their life or the life of their family at immediate risk. This is the reason why even in the late 20th century, a coal miner would risk their life every day in a coal mine, and die early of silicosis – the alternative was that their family might starve. This is one of the reasons that paid organ donation is illegal in the UK and the US – whilst there are some people that despite being well off, might be comfortable selling one of their kidneys for several tens if not hundreds of thousands of pounds, there are many desperate people that would sell a kidney for a few hundred pounds, far below the market rate, because that money would allow them to live a few more weeks. This is also one of the key reasons that many people view legal prostitution as morally wrong – even if the person has not been trafficked, and is not providing these services against their will, there is still the possibility that they are being forced into it by their poverty. Only when we can be sure that no-one is being coerced into these situations, can we be sure that there is no ethical issue with the libertarian argument that people should be able to do anything that doesn’t negatively impact someone else.

It is often a stipulation of state benefit systems that people must be willing to take any jobs that they are qualified for. This means that if something were considered a viable job, but you were unwilling to do it, you would not be eligible for benefits. Whilst this might at first seem reasonable – “why should the government pay for someone that considers themselves above working in a fast food restaurant?”, this allows people to be coerced into jobs that are less benign. Should someone today be in the situation of a coal miner 50 years ago, forced to work in conditions they perceive to be unsafe, to provide for their family? To go even further, if prostitution were fully legalised, should benefits be denied to someone that refuses to go into that line of work? Clearly not, and yet all of these exceptions require further policing, checking and bureaucracy, else they become accidental by-products of ill-conceived legislation.

This therefore is the benefit of a Universal Basic Income: under such a system, this robust safety net would ensure that no-one was being “price gouged”, as no-one’s life would be in immediate danger. This would then remove some (though perhaps not all) of the obstacles in the way of a truly libertarian society. Of course, in a similar vein to the Capitalist argument, this would likely result in dangerous jobs paying more, increasing the drive for safety, as the only people willing to work such jobs would be people that hadn’t been coerced. Without coercion, people are generally disinclined to risk their lives without significant reward. As Bertrand Russell wrote:

“Anarchism has the advantage as regards liberty, Socialism as regards the inducement to work. Can we not find a method of combining these two advantages? It seems to me that we can.” … “Stated in more familiar terms, the plan we are advocating amounts essentially to this: that a certain small income, sufficient for necessaries, should be secured to all, whether they work or not, and that a larger income – as much larger as might be warranted by the total amount of commodities produced – should be given to those who are willing to engage in some work which the community recognizes as useful.”

In ensuring that a base level of income is maintained, we can allow a far greater level of freedom in society than could be sustained without it.

Of course, how a Universal Basic Income is funded may change how libertarian it can be considered to be. An income tax for example, as proposed in the Accountant section is perhaps not the method a libertarian would prefer. It is however a fact that in most developed countries there is an income tax already, and that doesn’t look likely to change in the near future. As such, it seems a worthwhile policy to employ, given the ethical quandaries it avoids.

The Liberal: Less Vilification of the Poor

A common attack levied against people at the lower end of the income spectrum, ultimately used to justify cutting state benefits, is that of benefit fraud. People affording lavish lifestyles funded entirely by the state, or people sneakily augmenting this income by working a few hours cash-in-hand. This spectre serves to drive wedges between the rich and the poor, and to tarnish all people down on their luck as lazy, scheming and probably criminal to boot. The argument that your hard-earned taxes are going towards buying a family of nine a second widescreen TV can be both emotive and hard to refute. Despite the fact that this kind of occurrence is very rare, there will always be someone that manages to do it somehow, and when they are caught, it will spur yet another wave of anti-poor vitriol.

The beauty of the Universal Basic Income concept is that it is not possible to cheat. Everyone receives it, so it doesn’t matter whether someone is working on the side. This removes one of the main targets of criticism for low income families, and stops the insinuation of dishonesty amongst the poor. Furthermore, the fact that it leaves no holes in the safety net, means that as long as it is enough to survive on, there is no justification for theft. People may currently see someone poor as suspicious, knowing that they may be struggling to get by, and wondering how willing they might be to steal something to ease their desperation. Anyone stealing in a society with a Universal Basic Income would be doing so purely out of greed, which is not particularly correlated with poverty. In time this would hopefully reduce the conflation of poor with criminal that is so pervasive in our society.

Taking it further, people with nothing to lose can be driven to do terrible things. It is small wonder that the majority of people that become radicalised are from neighbourhoods with high levels of poverty. These people have a difficult existence, and can be exploited by anyone able to promise an improvement, or someone to blame, no matter how intangible or unrealistic this improvement may be. By giving everyone a Universal Basic Income, their existence becomes less fragile – they are no longer at risk of losing their state income through some bureaucratic confusion or technicality, which is an enormous source of stress for people in this situation. This gives people a better and less stressful existence, which is something that they would lose by going to prison or dying. The desire not to lose this more comfortable existence would vastly reduce the ease with which they could be radicalised into throwing their life away to further someone else’s agenda.

Any argument to reduce the Universal Basic Income would affect the wealthy too, making enthusiasm for reducing it likely to be lukewarm at best. The universality of the Basic Income plays into the common refrain of equality used to argue against progressive taxes: the question of why the rich should pay a higher percentage of their income, when they already pay more than someone less well off. Under the proposed system in the “Accountant” section there is a flat tax rate, therefore if everyone, rich and poor, receives the same income from the government and pays the same rate of tax, there can be no accusation of unfairness from influential wealthy people. The progressive effective tax rate is a natural consequence of the structure of the system, rather than a result of many arbitrary variables that evoke accusations of “class war”. Universal Basic Income also reduces the stigma associated with claiming state assistance – if everyone receives it, it is no longer a symbol of abject poverty, and is instead just a perk of being a member of the society. This would give a sense of solidarity between the rich and the poor – changes would benefit both or harm both, rather than being a divisive talking point.

When someone quits their job to write a book, we applaud them, championing their courage and their independent spirit. When someone is unemployed however, society tends to look down upon them, suggesting that it is almost unthinkable that they could accomplish anything worthwhile. This imbalance in perception between the worthiness of the “leisure class”, that can afford to spend time exploring their interests, and the hopelessness of the unemployed whose spare time is deemed to be wasted, could be redressed by a Universal Basic Income removing the stigma surrounding the unemployed. After all, if someone writes a book that is not very good, do we deem them to have wasted their time? Possibly, but we still applaud their efforts. Can someone unemployed have ideas and strive to put them into practice? Yes, but we are disinclined to give them the benefit of the doubt, and if it looks like they might make money from it, we tend to snatch their income away.

Equality of opportunity is a much sought after quality in society, and yet education, which is often the key to opportunity is so frequently out of the reach of people with low incomes. Attending a university away from the parental home can be prohibitively expensive, even before fees are considered, as accommodation and living costs tend to be significant, and require either debt or parental support. Without parents that can afford to pay these costs, students must either take on debt, or attend a university closer to home that may not offer the course that they want to do. By providing a Universal Basic Income to every adult, university students automatically qualify, and can therefore seek out accommodation in whichever city they see fit. All too often in the past, wealthy parents that have not seen the value of university education have denied their children the opportunity to go, by refusing to help them with these costs. These students, unlike their less well-off contemporaries, were ineligible for any grants, as the state assumed that their parents would pay. They were therefore less free to pursue the futures that could have been open to them. By treating individuals as individuals, and not adjusting state assistance based on the wealth of someone’s parents, it ensures that people do not end up being denied opportunities despite being in a seemingly more privileged position.

More than this however, a Universal Basic Income allows anyone at any time of their life to seek out further training, education or experience. Because they can be assured that they will have enough money to survive, people can leave their employment, enrol in training, and better themselves without needing to spend years saving up to be able to afford to not work for a few months. This should drastically improve social mobility, enabling interested and motivated people to gain the skills they need to become successful.

The Socialist: A Robust Safety Net

One of the main issues with social safety nets as they stand currently is known as the “Poverty Trap”. This is the phenomenon whereby benefits are curtailed when someone finds a job, in such a way that they are worse off than before. This can happen in several different ways – either the reduction in benefits occurs at the same rate or faster than the increase in job related income, meaning that the additional time (and opportunity cost) spent working has either zero or negative net effect on income. Alternatively, some benefits are removed entirely when a job is found, which is detrimental when that job is part time or a “zero-hours contract”, again resulting in a lower income than before. This kind of benefit structure actively discourages people to find jobs, as unless they are able to walk into a reasonably paid, full time position, they are better off unemployed. This then means that unless they can weather a period of even lower financial security, they are not able to gain work experience to enable them to seek better jobs.

Clearly operating a financial safety net in this way does discourage people to find new work, however a guaranteed income which does not drop off when income is earned, does not fall into this trap – every extra bit of income earned has a net positive effect on their living situation and finances. The argument could be made that being able to survive off a Universal Basic Income, that had no requirements attached regarding proving that you are seeking work, might still discourage people to find new work, but this denies the tendency of people to desire to improve their position. There will undoubtedly be some people that are content with a small but adequate income, allowing them to survive but little else, however most people aim for more – more comfort, more interest, more hobbies or more education.

The requirement in current systems to prove that you are seeking work is perhaps well intentioned, but ultimately a misguided and bureaucratic solution to the issue of unemployment. More time and effort are required to satisfy these conditions, than would be required to simply look for a job, and the risk of losing this benefit, if these conditions are not met is a constant concern for people in this situation. This can lead to anxiety and mental health issues, as well as people that fall through the gaps either through an inability to fill out the paperwork correctly, or through not meeting a particular eligibility requirement.

The problem of people falling through gaps in the safety net is a very serious one – one example of a well-intentioned but poorly thought out eligibility requirement is that people not be “voluntarily homeless”, to avoid people in shared accommodation exploiting the system to be able to get “their own place”. The issue here is when someone (often teenagers) is in a difficult home situation, they may choose to leave for their own safety or sanity. If they chose to leave, and were not thrown out of the house however, they are deemed to be “voluntarily homeless”, and therefore are ineligible for assistance with housing. This can lead to people remaining in dangerous home situations, when they would be better off leaving, ultimately putting themselves in danger because of their lack of financial independence. It could be argued that there exist shelters for some victims of domestic violence, which should allow people to escape these situations, however these are a stop-gap measure that cannot be relied upon by everyone (many do not admit young men), and still do not resolve the person’s issue of financial dependence.

The inability to successfully navigate the bureaucracy is another serious gap which many people can fall foul of. Even if support is provided to people that are unable to read, have hearing difficulty or have difficulty understanding the forms required, this support suffers from mixed motivation – ensuring that people don’t get money that don’t meet the criteria, whilst helping people to express the criteria that they have met. These diametrically opposed objectives will inevitably conflict, and either lead to accusations that support staff are “helping people to cheat the system”, or that they are “exploiting the vulnerable to cut costs”. By cutting out assessment, and providing a Universal Basic Income to every citizen regardless of employment status or job-seeking activity, it removes this bureaucracy, thus avoiding this conflict. This ensures that regardless of the specific nuances surrounding a person’s financial distress, the safety net is guaranteed to function, and not miss a single person in need.

The Capitalist: Removal of Market Distortion

It is a frequently made argument, that minimum wages distort the market. Either forcing companies to pay more for a certain activity than it is really worth to them, or rendering someone unemployable if their skills are not worth the minimum wage that a company is allowed to pay. This is an unavoidable negative consequence of a minimum wage law, yet without it, companies would be allowed to pay many people so little that they would struggle to survive. After all, what is their alternative – if no-one is willing to pay them any more money, their only other option is to not work, and either live off state benefits, or starve. The provision of Universal Basic Income would mean that everyone was able to survive, and could then augment their earnings with additional employment income. This would remove the requirement for a minimum wage, as everyone would have enough income to survive, which would then free up the companies to pay the market rate for the work they required.

This leads to the obvious objection – “wouldn’t companies use this as an excuse to drop pay for all workers?”, however because a Universal Basic Income is not dependent on whether someone has a job, or has recently chosen to leave a job they were unhappy with, people are not held hostage by the companies they work for – no-one has to work just to survive, so if people feel that they are not being paid a fair amount for their work, they are free to leave. This freedom should also reduce the inertia stopping people from moving between jobs, which is another distortion in the market. When you move jobs, there is often a probation period, so you are potentially leaving a secure position, where it would be expensive for the company to make you redundant, and moving to a position where you could be laid off with very little difficulty, and almost no severance package, leaving you in a very fragile position. With the safety net of a Universal Basic Income, you know that your income cannot drop below a certain level, making the risk less severe. This should make people feel able to move jobs with less risk to their personal finances and wellbeing, which should make the job market more efficient.

The ability of people to survive without a job, without the demeaning process of jumping through a series of bureaucratic hoops, and without the pressure to take any job that is offered, no matter how uncomfortable they are with it will also empower people in other ways. They will be able to turn down jobs offering poor working conditions, and if enough people are disinclined to work under such conditions, this will incentivise employers to improve them. Mindless or unpleasant jobs would also likely have to pay more to encourage people to do them, which would increase the drive for automation. Flexible working is a popular concept, that companies could find it beneficial to offer, as it would increase the size of the employment pool that they have access to – forcing people to work full-time or not at all would no longer be viable if people could afford to pick the latter option. All of this effectively levels the playing field between companies and employees, giving rise to a much freer and less distorted market.

Some might be inclined to say that a Universal Basic Income reduces the link between merit and reward, which is itself a market distortion, however it does not affect this link very much at all, by the very nature of its universality. Unlike other state benefit systems that reduce as incomes increase, thereby reducing the reward of incremental merit, the universality of a Universal Basic Income means that being paid by someone will necessarily increase your income, but that there is a base level below which it is not possible to fall. The link between merit and reward was outlined by John Stuart Mill:

“This System does not contemplate the abolition of private property, nor even of inheritance; on the contrary, it avowedly takes into consideration, as elements in the distribution of the produce, capital as well as labour.” … “In the distribution, a certain minimum is first assigned for the subsistence of every member of the community, whether capable or not of labour. The remainder of the produce is shared in certain proportions, to be determined beforehand, among the three elements, Labour, Capital, and Talent.”

The capitalist would argue that the market is the best way of distributing this remainder, according to the value of the labour, capital and talent brought to bear by each individual. This approach allows the market to do just that, whilst minimising the interference required to create a society that is still able to provide for all.

The Entrepreneur: More Stability

Entrepreneurialism is a risky business – most start-ups fail, losing the entrepreneur money, and yet as a whole, it is a process that is hugely beneficial for the economy, as it generates significant employment and innovation. Unfortunately, this tendency to fail makes entrepreneurialism something that most people cannot risk. If you are not already fairly wealthy, leaving a job to pursue an idea that may or may not generate any income is unaffordable right from the start. Even for people with some money behind them, it can be difficult to make ends meet in the period between the initial capital outlay and when the company becomes revenue generating.

Ordinarily, state benefits would not cover someone that had left their job to start a business, however these people are often placed in very difficult positions. They could be faced with the choice between giving up on their idea, which might be on the verge of success, losing all of the investment they have put in, or trying to keep it going whilst living in effective poverty until revenue starts coming in. This decision is a difficult one, and it is often not entirely trivial to just walk into a job straight away after things do fall apart. This can leave some entrepreneurs with an employment gap, and it can take some time for the state benefits to start to come in.

The advantage of a Universal Basic Income here is that it would both avoid this income gap, and help them to succeed. In the event of the worst case scenario, it would ensure that there was no period in which the entrepreneur had no income and therefore there would be no risk of falling into extreme poverty as a result of trying to start a business. On the other hand, while running the business, it would ensure that even if the company had a period of very low or no revenue, the entrepreneur could still eat, would not risk homelessness, and would be able to focus on making the business a success without worrying about either of these things.

Furthermore, a Universal Basic Income would open entrepreneurialism up to people with lower incomes, and less money behind them, as they similarly would not be risking losing their homes. It is a phenomenon that was observed when a Universal Basic Income was trialled on a small scale in a village in Namibia between 2008 and 2012: not only did the number of children in education increase and malnutrition decrease, but several people that were below the poverty line before the trial, started small businesses and were able to increase their earnings considerably once they had the small amount of Universal Basic Income available to them. Through providing greater stability, the Universal Basic Income grants people the freedom to take more risks, which would otherwise have the potential to ruin them.

Various charities have had similar initial results trialling microfinance programs in villages in Africa, and it is true that easy access to debt does encourage more people to try to start a business, however the longer-term impact of these schemes was not so positive. As is to be expected, only some of the small businesses set up were successful, leaving many in the community as poor as before, but also saddled with debt. Those who used microfinance to improve their living conditions likewise only saw a temporary benefit, as they had not increased their earning ability by the time the repayments started to bite. The benefit of a Universal Basic Income over such microfinance or “loans for the poor” initiatives is that low-income people who use this money to start a business will be no worse off than before, if their business fails.

Alongside actors, musicians and artists in general, the existence of various “cottage industries” is a testament to people’s desire to make a business out of their passion. They may not be scalable, relying on very specific people and skills, or they may have a small target market, but they make the economy more diverse, and arguably more flexible. Making it easier and less risky for people to choose to be artists or craftspeople is likely to be a boon to the creative industry in general and will allow more people from a wider variety of socioeconomic backgrounds to follow their passion.

The enthusiasm with which people embrace the idea of “being their own boss”, is a very good counterargument against the idea that a Universal Basic Income will encourage people to stop working. Undoubtedly some people will be happy to live the meagre existence provided for by such a policy, but most people tend to strive for more. Giving people the ability to take risks, without suffering catastrophic consequences is highly likely to result in improved innovation. This might mean that some people quit their jobs, but many of these will do this to try their hand at something new and entrepreneurial, rather than to simply sit at home doing nothing.

The Economist: Effective Stimulus

One of the problems with the economy as it stands is the positive feedback loop of recessions. When times are good, things work well: people spend money, which allows businesses to pay their staff, who can then spend their money and so on. Every pound or dollar spent flows around the economy several times, facilitating growth and prosperity. When the economy slows however, people see hard times ahead, and will try to save money, reducing their expenditure, which in turn reduces businesses’ income. These businesses feel the squeeze and may lay off staff, who then have even less money to spare, exacerbating the problem, reducing the flow of money and making a recession more likely. The concept of a stimulus is an idea originally thought up by the economist John Maynard Keynes: the government can inject money into the system, often by funding large infrastructure programmes, or more recently by giving it to banks to lend out. This has the effect of increasing the flow of money again, with the hope that this will kick-start the economy, improve employment, and get things back to normal.

The issue with this idea, is in the implementation – when should the stimulus be made, and who should receive it? Recent stimuli have been a windfall for the banking sector, raising questions around corruption and impropriety, while previous stimuli aimed at investing in infrastructure have raised questions about efficiency and government waste. There is also the risk that the stimulus may be implemented too late, allowing the recession to bite before any action is taken, or may be implemented for too long, resulting in too much money flowing around the economy, causing higher inflation. In principle, stimuli should be counter-cyclical – that is, when the flow of money around the economy falls, they should be used to increase it, and when the flow of money around the economy rises again, they should stop. Unfortunately, stimuli inevitably become political, which hampers the objectivity with which they can be applied.

It is a well understood and intuitive phenomenon that poor people spend a higher proportion of their income than the rich. People with high incomes can afford to save, whereas people living on the bread-line spend everything they receive, just to make it through the day. The beauty of a Universal Basic Income is that this phenomenon makes it a self-adjusting pseudo-stimulus (it is not technically a stimulus in the strictest sense as it is moving existing money, not adding additional money to the system). As the economy contracts, and people become poorer, the Universal Basic Income becomes a more significant part of their income, and they will spend a higher proportion of it. Equally, as the economy improves, fewer people will be dependent on the Universal Basic Income, so it will be more likely to be saved rather than spent, avoiding the economy becoming overheated. This means that if an economic slow-down occurs, resulting in many job losses, there is still a large amount of cash flowing into the economy from the people spending this Universal Basic Income, which should keep many businesses afloat, and reduce the cascade effect of further job losses.

Due to the fact that both demand and investment fall during a recession, there is a choice to be made between propping up demand and propping up investment when considering ways to mitigate the economic damage. Propping up investment is obviously intended to encourage higher employment, which will in time give people more money, and therefore increased demand. As was seen in the recent recession in the UK however, despite improved access to investment through cheap rates of borrowing, companies can take a long time to translate the increased availability of investment into higher employment. This is something of a self-fulfilling prophecy – they don’t want to increase their employment until demand improves, and demand won’t improve until employment increases. This situation does not persist indefinitely, but does act as a kind of “friction”, slowing down the impact of the policy.

Propping up demand on the other hand removes the disincentive for companies to utilise any investment they have access to – there may well be less investment available, but what there is, is more likely to be used for increasing employment. Low investment is not ideal, but here the “friction” is on our side – a short period of low investment means that new machinery will not be purchased, and old machinery will not be replaced, however this will simply result in people sweating their assets. It is only if this low investment persists, that significant permanent reductions in capital stock will emerge. As such, a Universal Basic Income props up demand without needing an actual stimulus – investment will reduce, but a vicious self-reinforcing cycle of collapsing demand is avoided, and due to the “friction” around investment, if the economy recovers relatively quickly, there shouldn’t be too much lasting damage.

If an actual stimulus is still required, the Universal Basic Income provides a highly efficient vector for the stimulus money – rather than government spending on infrastructure or lending to banks, the Universal Basic Income can simply be temporarily increased, providing a wealth transfer to every citizen in the country. This avoids any questions of inefficient government spending or impropriety, by avoiding the government picking favourites. Instead, as wealth is distributed in such a way that there are usually many people at the lower end of the wealth spectrum for every person at the higher end, the vast majority of the stimulus goes directly to people that will spend most of it, providing an immediate and effective injection of cash into all of the most critical businesses.

A common perception around a Universal Basic Income is that it would cause higher inflation, similar to what occurs when a stimulus is applied when one is not required, however this is unlikely to be the case. Unlike cheap bank loans, which increase the supply of money for businesses, or the government printing money to spend on infrastructure, a Universal Basic Income does not require creating money, as demonstrated in the Accountant section. It is the act of creating more money either through printing or through debt that is inflationary.

When looking at housing specifically, rather than the economy as a whole, it can be argued that a Universal Basic Income could drive an increase in housing costs, however this is also the case with any effective system of benefits: if there is an inelastic supply of a good, the price will necessarily rise to keep consumption the same level as before. If there are not enough houses for the number of people in the country, there is no way to house everyone. Eventually one might expect that higher prices would lure more competitors into the market, increasing supply, but this is dependent on the availability of land and the planning regulations. Ultimately this is a problem of housing policy, with no “silver bullet”. That being said, a Universal Basic Income does have one advantage in this area that other benefit systems lack – unlike programs such as housing benefit or social housing, Universal Basic Income does not tie you to a location. If you have no job, you can move to an area where housing is cheap, rather than relying on the government getting around to building council housing in London. This does depend on the Universal Basic Income being both implemented nationally and administered nationally, as having to re-register for benefits after moving to a different area often causes a discontinuity in payments, which can be hugely problematic for people. This is a reasonable condition to expect though, if it is being administered through the tax code.

One of the most widely used arguments for a Universal Basic Income since the advent of computers and robotics is that of automation. As more and more jobs become automated, reducing the need for human employees, more people will become unemployed, and possibly unemployable. It remains to be seen whether this will be the case, as previous technological advancements have simply led to higher production volumes, lower costs and higher demand. Needless to say, these disruptive technologies caused a temporary dip in employment while the market rearranged itself, and people trained for new roles. Even if large scale automation does not result in fewer jobs to go around, it will cause temporary unemployment on a large scale, which will have inevitable negative consequences without a system in place to ease the impact of this loss of income. Current state benefit systems, by virtue of their piecemeal approach, leave too many gaps to fall through, and do not adequately encourage retraining, demanding that people constantly apply for jobs that may be dwindling in number, rather than allowing them the time to train in another field where more jobs are becoming available.

If large scale automation does result in a permanent reduction in the number of jobs required by human workers, it is highly likely that existing systems of administration for state benefits would become overloaded. Providing everyone with the means to survive by implementing a Universal Basic Income is likely to be far more straightforward than scaling up the existing system by an order of magnitude. Because people would no longer need a full-time job in order to have enough money to survive, this could also result in the remaining jobs being divided up and spread across more people, so that everyone could still augment their Universal Basic Income, but could work fewer hours per week.

The Philosopher: The Land Dividend

In the depths of pre-history, before all of the land in the world was parcelled up and owned by individuals and organisations, the human population was quite low, and it was possible for a stone-age human to hunt, forage and maybe even subsistence farm on some land to eke out a meagre existence. Life was hard, the margin of error was thin, a bad winter or a poor harvest could be fatal; yet in this anarchist’s dream world, unless another marauding tribe came to drive you away, you could live on and extract as much wealth from this land as you were able or inclined to.

In modern times, if you are unlucky enough to be born into a family that does not own land, you do not have the right to any land to live on or extract wealth from. You may rent some land to live on, if there is something you can do that someone is willing to pay you for, but if there is not, and you find yourself ineligible somehow for whatever “state assistance” may be provided, there is no longer the fall-back option of subsistence. There exists common land, but in most areas it is illegal or at the very least frowned upon to try to live on it or extract wealth from it. Unable to rent a place to sleep, not permitted to erect any effective form of shelter such as a tent, with no land to cultivate and with increasing restrictions on even their ability to scavenge, a modern homeless person lives a far more fragile existence than they might have found had they lived ten thousand years ago.

It is unreasonable to expect every step of progress to be a “Pareto improvement” (a change which results in everything either staying the same or improving, with nothing at all getting worse), for instance environmental regulations may save lives and be a vast improvement for society over all, but some companies will inevitably lose out, and some people may lose their jobs. Pareto improvements are indeed very rare, but an example of somewhere you might expect a Pareto improvement is in the change between your prospects had you lived ten thousand years ago, and your prospects now. Is it so unreasonable to hope that a human born into the world today would, if not be better off, at least never be worse off than they would have been, had they been born in the stone-age? If modern society cannot even make a Pareto improvement to stone-age society, we must be doing something wrong, and yet for the person sleeping huddled in a doorway, with just a few damp sheets of cardboard to protect them from the blustery December wind, being awoken and moved along every few hours by security guards or the police; it is hard to see a cave with a fire, or a bivouac in the forest as anything but an improvement.

The key issue is that the population of humans is increasing, but the supply of land is not. Although owning land may not be the best way to make a quick buck, those families that managed to gain ownership of some land have, over the course of a couple of hundred years, become exceedingly wealthy. The lack of land available for the increasing number of remaining people, combined with the low cost of holding onto land, and the requirement of everyone to have a place to live, gives rise to a very profitable situation for land owners. Yet in the stone-age, what rights did people have over the land? It simply existed – ownership is a fundamentally human concept, not a natural characteristic of anything.

As every human is an individual, and not just an extension of their parents, the question is, why should one have less land to sustain them, just because their parents had more children or less wealth? The only truly fair way to divide up the land in the world, that is so essential for survival, is for everyone to have the same worth of land as everyone else, as a birth-right (worth rather than area, as the area of desert required to sustain a human is significantly larger than the area of fertile pasture that is required). This is clearly impractical for a number of reasons: firstly, it would be a bureaucratic nightmare to manage, as every new person born would need to be allocated their plot of land, taking a small amount from everyone else; secondly, how would we accurately assess the worth of an area – desert is almost worthless, but in our modern society oil is a very valuable commodity – clearly land cannot be allocated based solely on its subsistence value, but equally desert with oil beneath it is still worthless to someone that doesn’t want to drill for oil.

Thankfully the solution to this problem is much simpler, due to the invention of money. Rather than explicitly dividing land between people according to its worth, a country can “own” all of its land on behalf of its citizens, and pay them all an equal rent or a “land dividend”, based on the total value of the land to the country. Now the only thing needed to make this a Pareto improvement over the stone-age, is for this “land dividend” to be enough money to be sure that you can avoid death from exposure or starvation. It does not necessarily have to cover a comfortable existence, but it needs to be enough to cover a place to live, heat, food and water. On the other hand, if it truly is a “land dividend”, this dividend should be reflective of the worth of that land, which in turn is reflective of the economic activity performed on the land, which could be much higher than just covering subsistence in a wealthy country.

If the “land dividend” is based on the concept that the country is holding the land in trust for all of its citizens, the government might want to charge rent (or more commonly referred to as a “Land Value Tax”) to anyone using land in the country. There might be a certain point, a particularly sized area of land, that could be rented by an individual from the government, that cost exactly the same amount as the “land dividend” that they were paid, resulting in no net payment to or from that individual. This individual, should they feel so inclined, could live like a cave-man, with very little interaction with the government, thus demonstrating incontrovertibly that a Pareto improvement had indeed been attained – at the very least they wouldn’t be better off, had they been born ten thousand years ago.

This can be considered an extension of the original argument made by Thomas Paine:

“It is a position not to be controverted, that the earth, in its natural, uncultivated state was, and ever would have continued to be, the common property of the human race.” … “it is the value of the improvement, only, and not the earth itself, that is in individual property. Every proprietor, therefore, of cultivated lands, owes to the community a ground-rent (for I know of no better term to express the idea) for the land which he holds; and it is from this ground-rent that the fund proposed in this plan is to issue.” … “to every person, rich or poor”, “because it is in lieu of the natural inheritance, which, as a right, belongs to every man, over and above the property he may have created, or inherited from those who did.”

Which whilst rather academic, does give us some very good principles to build on.

Conclusion: Implementation Possibilities

Having addressed the idea of a Universal Basic Income from a wide range of perspectives, it is hopefully not unthinkable that such a policy could generate a similarly wide base of support, given the right framing. If the same policy can appeal to socialists, capitalists, conservatives and liberals alike, whilst being both practical and affordable, it is clearly in need of more attention. The issue is, that it is quite a dramatic policy shift that would be politically untenable to achieve in one fell swoop.

It is understandable that people are wary of dramatic changes to policy, as such things can have unintended consequences that are difficult to predict and also difficult to reverse. The question then becomes how such a policy could be implemented in controlled stages, whilst both maintaining an acceptable level of public support, and avoiding creating an even more complicated system during the transition. This would avoid any sudden, large-scale changes, and therefore be more controllable, less risky and easier to reverse, should the need arise.

Thankfully, there is a way to gradually simplify the existing UK tax code, whilst making it converge with the system of Universal Basic Income described in the Accountant. This sequence of changes also leaves the benefits system largely untouched, simply applying to fewer and fewer people, as the transition progresses. I shall detail this potential sequence of policy changes, to demonstrate that it is indeed possible to achieve the end goal of a Universal Basic Income, without any dramatic changes that could cost excessive political capital, and expose the people and economy of the country to too much risk.

The first few steps do not introduce a Universal Basic Income at all, instead laying the groundwork for its introduction by simplifying the tax code. Starting with the existing 2018-19 UK tax code:

| £11,850 “Personal Allowance” not taxed |

| £11,850 to £46,350 taxed at 20% |

| £46,350 to £150,000 taxed at 40% |

| Anything above £150,000 taxed at 45% |

| For every £2 of income over £100,000, you lose £1 of “Personal Allowance”, which is therefore then taxed at 40% |

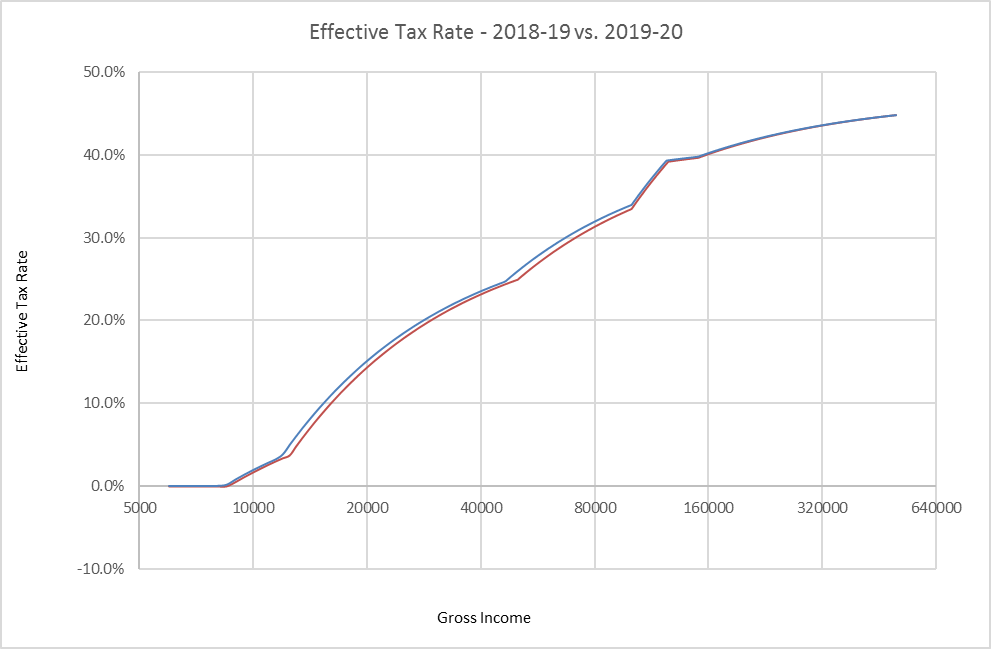

This was changed for the 2019-20 tax year. The structure of the tax code remained the same, but the numbers were made slightly friendlier, giving everyone a small tax cut:

| £12,500 “Personal Allowance” not taxed |

| £12,500 to £50,000 taxed at 20% |

| £50,000 to £150,000 taxed at 40% |

| Anything above £150,000 taxed at 45% |

| For every £2 of income over £100,000, you lose £1 of “Personal Allowance”, which is therefore then taxed at 40% |

After including the effects of National Insurance, which from 2018-19 to 2019-20 had its lower threshold changed from £8,400 to £8,600 and its upper threshold changed from £46,350 to £50,000, this made the effective tax rate graph change from the blue line to the red line below: